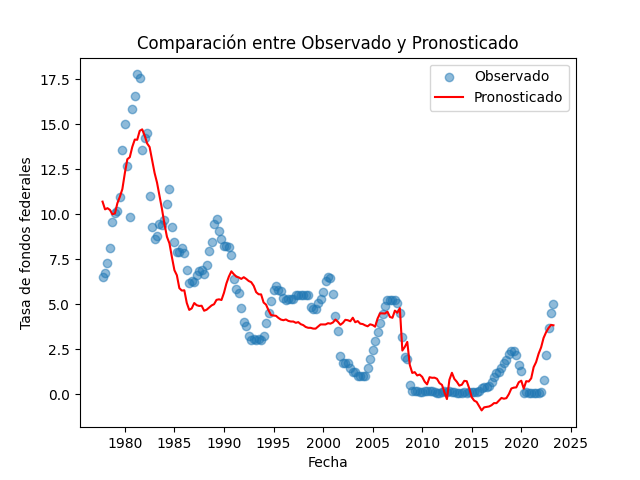

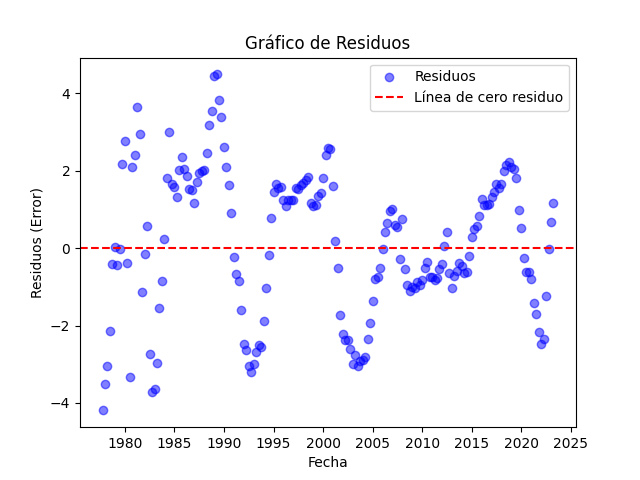

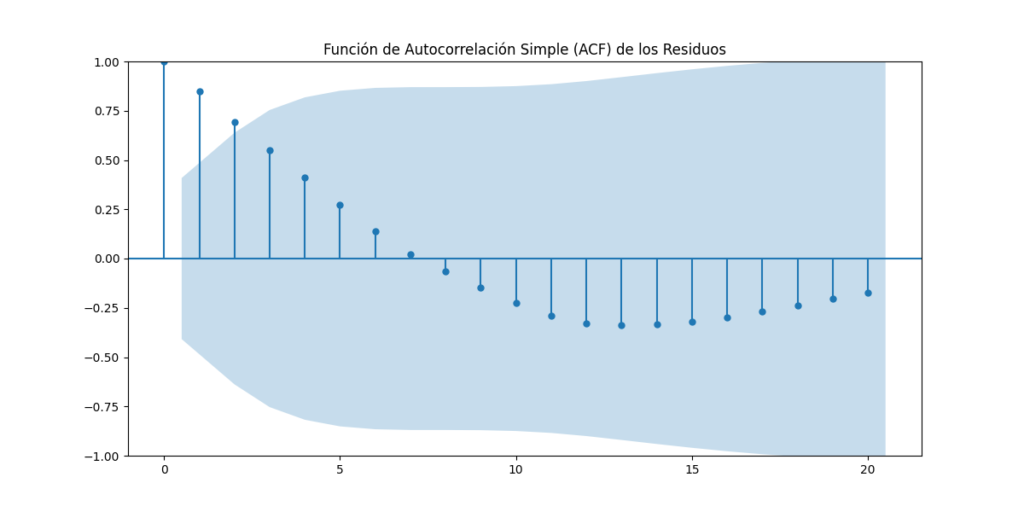

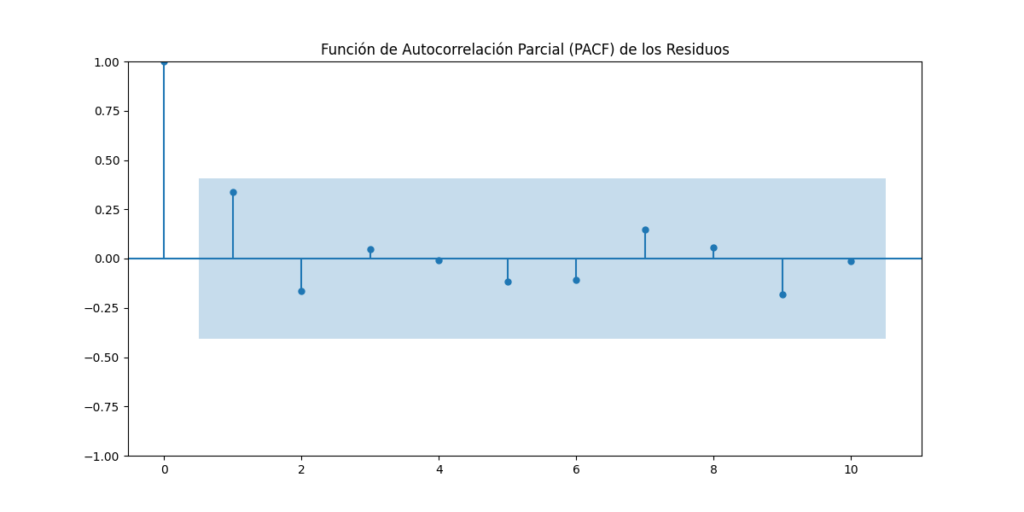

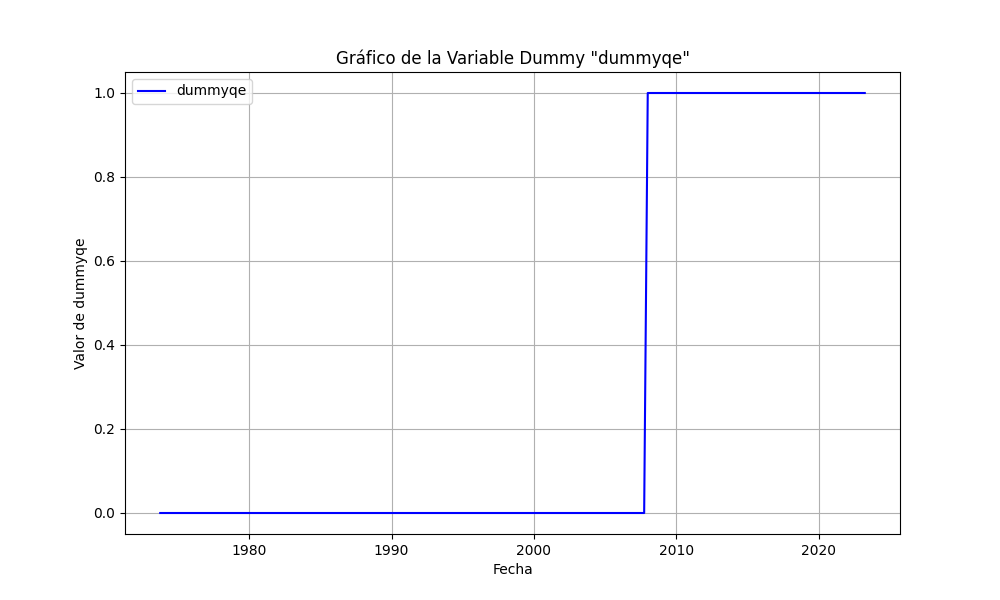

In this analysis, we utilized Python to delve into the monetary policy of the United States Federal Reserve from 1973 to 2023. Our primary objective was to uncover robust evidence regarding the relationship between the federal funds rate (fedfundsrate) and two fundamental components: the annual average growth rate of productivity and the annual average inflation rate, evaluated over 4-year periods. Additionally, we incorporated a key element: the inclusion of a dummy variable associated with Quantitative Easing (QE) or the expansion of the Fed’s balance sheet. This analysis was conducted using Python, and we conducted comprehensive tests to assess the model’s quality.

Key Findings:

- The Fed’s monetary policy responds uniquely to changes in productivity growth and inflation. A 1% increase in productivity growth prompts the Fed to raise its interest rate by 0.238637%, indicating a less than proportional response.

- On the other hand, a 1% increase in inflation leads to a 1.350490% increase in the Fed’s interest rate, implying a more than proportional response.

- Additionally, the dummy variable related to Quantitative Easing (QE) enhances the model’s R2 and estimators, underscoring its significance in monetary policy.

The interpretation of these findings suggests that the Fed aims to allow private portfolios to partly reflect societal advancements in productivity. Furthermore, the Fed’s response to increases in inflation can be seen as an attempt to offset long-term purchasing power losses and influence aggregate demand to control inflation.

These results also support the idea that the Fed follows a monetary policy rule similar to the Pasinetti Interest Rate Rule. However, it’s essential to recognize that economic reality is highly complex, and the Fed’s decisions can have significant implications for the overall economy. For instance, if rents surge in response to interest rate hikes, if increases in production costs due to higher credit costs are passed on to consumers, or, more importantly, if substantial government interest payments end up financing consumption.

Understanding these channels, through which an interest rate increase not only exerts downward but also upward pressure on inflation, is crucial. This takes on particular importance in light of the demographic profile of American savers, which may correlate with a higher marginal propensity to consume compared to savers in other parts of the world (see Warren Mosler).

Robust linear Model Regression Results

==============================================================================

Dep. Variable: fedfundsrate No. Observations: 183

Model: RLM Df Residuals: 180

Method: IRLS Df Model: 2

Norm: HuberT

Scale Est.: mad

Cov Type: H1

Date: Wed, 11 Oct 2023

Time: 22:05:51

No. Iterations: 17

==============================================================================

coef std err z P>|z| [0.025 0.975]

------------------------------------------------------------------------------

Deltapr 23.8637 10.801 2.209 0.027 2.695 45.033

Deltacpi 135.0490 4.329 31.196 0.000 126.564 143.534

dummyqe -2.4010 0.283 -8.493 0.000 -2.955 -1.847

==============================================================================

R-squared: 0.8705¡Ya en Amazon!

¡No pierdas esta oportunidad única y limitada para obtener un 50% de descuento en el precio original del programa de cursos asociado a 'CAMINO A LA RIQUEZA'! Utiliza el código 'caminoalariqueza' al momento de la compra y asegura tu cupón de descuento exclusivo para lectores del libro. Esta oferta de descuento estará disponible de manera intermitente en el tiempo, por lo que es mejor aprovecharlo ahora mismo. Adquiere las herramientas necesarias y emprende tu camino hacia la riqueza financiera antes de que sea demasiado tarde. ¡No te quedes fuera de esta oportunidad imperdible!

¡Emprende tu camino hacia la riqueza ahora!